International Standard on Quality Management 1 (hereinafter “ISQM 1”) Quality Management for Firms that Perform Audits or Reviews of Financial Statements or Other Assurance or Related Services Engagements is effective from 15 December 2022. ISQM 1 has replaced the audit quality control standards, International Standard on Quality Control 1 (hereinafter “ISQC 1”) Quality Control for Firms that Perform Audit and Reviews of Historical Financial Information, and Other Assurance and Related Services Engagements. The implementation of ISQM 1 is applicable to ALL firms that perform audits or reviews of financial statements or other assurance or related services engagements.

QUALITY has been prioritised for auditors especially higher audit risks being created where remote working is allowed during COVID-19 lockdown. ISQM 1 requires a firm to design, implement and operate a system of quality management for audits or reviews of financial statements, or other assurance or related services engagements. Furthermore, the firm is also responsible to evaluate the system of quality management within one year following 15 December 2022 as required by ISQM 1 to ensure the quality management is operating effectively or any weaknesses being identified throughout the year.

The implementation of ISQM 1 can be a challenge to small medium audit firms where a system of quality management needs to be in place. From another perspective, it can be a good opportunity to collaborate between the small medium firms to conduct more rigorous cold file review on a yearly basis (at least) to improve on the audit quality among the firms.

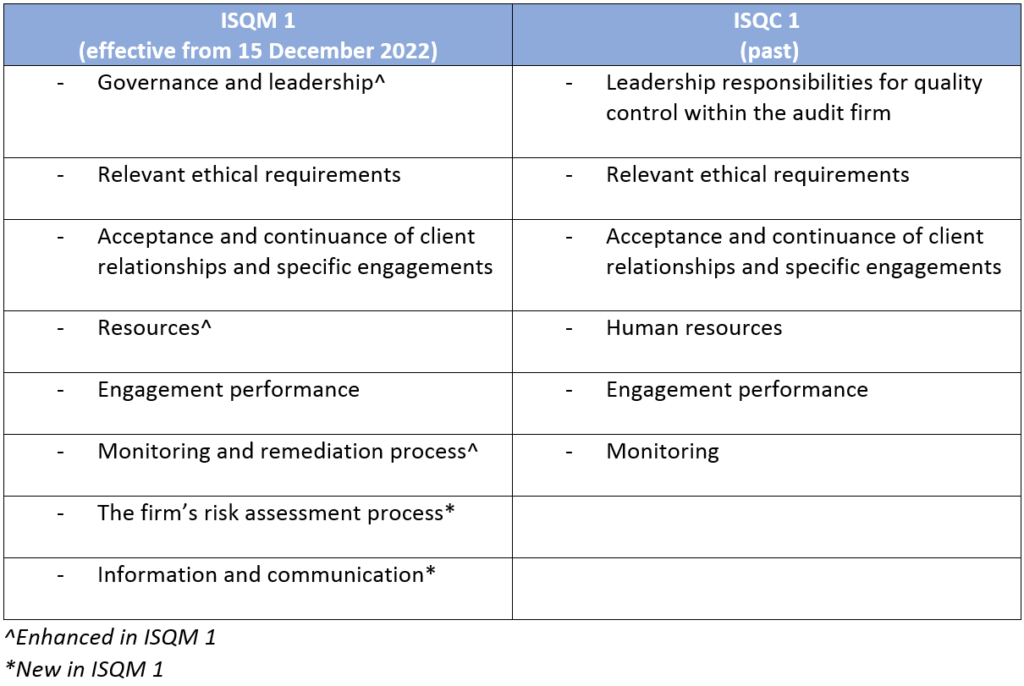

Before we go into the details of ISQM 1, let’s see the comparison of the eight components of ISQM 1 and six elements of ISQC 1. The components of ISQM 1 are aligned to the six elements in extant ISQC 1 and include two new components, the firm’s risk assessment process and information and communication.