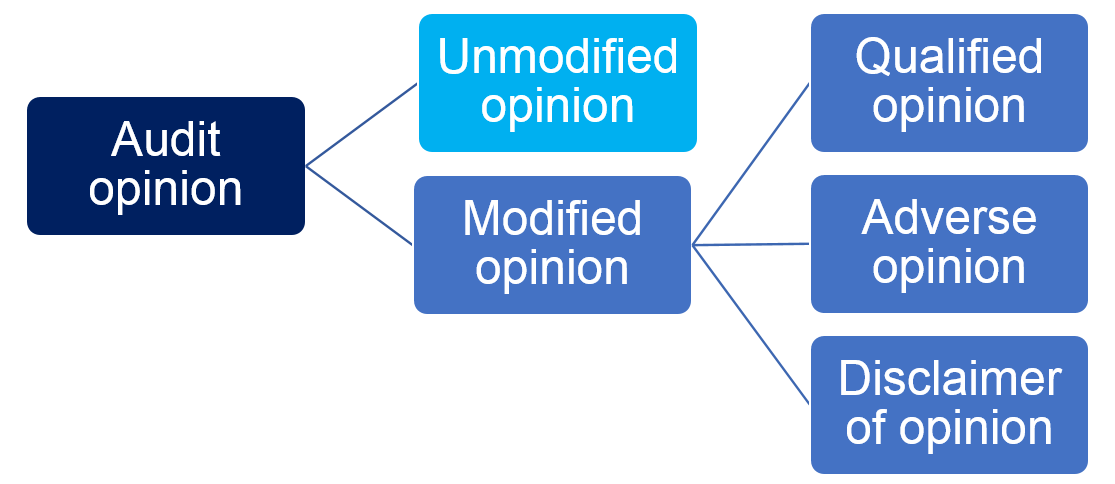

What is an Auditor’s Opinion?

An auditor’s opinion is a formal statement made by an auditor concerning a client’s financial statements. There 4 types of audit opinion which can see from the flow chart below:

Unmodified Audit Opinion

Unqualified Opinion

The auditor is satisfactory concluded that the financial statements are free from material misstatements and express the financial statements give a true and fair view.

Unmodified opinion – Material Uncertainty Related to Going Concern

– This separate section applies if the auditor has concluded that a material uncertainty related to going concern exists, and for which adequate disclosure has been made in the financial statements. This section will draw attention to the note in the financial statements that discloses this matter and state that these events or conditions indicate that a material uncertainty exists that may cast significant doubt on the company’s ability to continue as a going concern. It will also state that the auditor’s opinion is not modified in respect of the matter.

– Examples of events of conditions:

Financial

- Net liability or net current liability position

- Fixed-term borrowings approaching maturity without realistic prospects of renewal or repayment; or excessive reliance on short-term borrowings to finance long-term assets.

- Indications of withdrawal of financial support by creditors.

- Negative operating cash flows indicated by historical or prospective financial statements.

- Adverse key financial ratios.

Operating

- Management intentions to liquidate the entity or to cease operations.

- Loss of key management without replacement.

- Loss of a major market, key customer(s), franchise, license, or principal supplier(s).

- Labor difficulties.

- Shortages of important supplies.

Others

- Non-compliance with capital or other statutory or regulatory requirements, such as solvency or liquidity requirements for financial institutions.

- Pending legal or regulatory proceedings against the entity that may, if successful, result in claims that the entity is unlikely to be able to satisfy.

- Changes in law or regulation or government policy expected to adversely affect the entity.

- Uninsured or underinsured catastrophes when they occur.

Example:

Material Uncertainty Related to Going Concern

We draw attention to Note XX in the financial statements, which indicates that the Company incurred a net loss of RMXXX during the year ended 31 December 20XX and, as of that date, the Company’s current current liabilities exceeded its current assets by RMXXX. As stated in Note XX, these events or conditions, along with other matters as set forth in Note XX, indicate that a material uncertainty exists that may cast significant doubt on the Company’s ability to continue as a going concern. Our opinion is not modified in respect of this matter.

[MIA: RPG 12 Auditors’ report on financial statements prepared in accordance with Malaysian Private Entities Reporting Standard (MPERS)]

Modified Audit Opinion

There are two circumstances when the auditor may choose to issue a modified opinion:

- When the financial statements are not free from material misstatement or

- When they have been unable to obtain sufficient appropriate evidence.

Circumstance (1): Financial statements are materially misstated

A material misstatement of the financial statements may arise in relation to:

(a) The appropriateness of the selected accounting policies;

(b) The application of the selected accounting policies; or

(c) The appropriateness or adequacy of disclosures in the financial statements.

Qualified opinion (with ‘except for’ paragraph)

– The auditor agrees with the rest of the financial statements but disagrees with that particular element of them.

– In this situation the auditor will qualify the audit with an ‘except for’ paragraph (e.g.: In our opinion, except for the effect on the financial statements of the matter referred to in the preceding paragraph, the financial statements give a true and fair view.)

Adverse opinion

– A disagreement which is material and pervasive is of such significance that the financial statements do not give a true and fair view.

– In such a situation an adverse opinion is issued (e.g.: the financial statements do not give a true and fair view.)

Circumstance (2): Insufficient appropriate audit evidence

Insufficient appropriate audit evidence (also referred to as a limitation on the scope of the audit) may arise from:

(a) Circumstances beyond the control of the entity;

(b) Circumstances relating to the nature or timing of the auditor’s work; or

(c) Limitations imposed by management.

Qualified opinion (with ‘except for’ paragraph)

– A material insufficient evidence which mean that the auditor agrees with the rest of the financial statements but is unable to agree with that particular element of them.

– In this situation the auditor will qualify the audit with an ‘except for’ paragraph (e.g.: In our opinion, except for the matter referred to in the preceding paragraph, the financial statements give a true and fair view)

Disclaimer of opinion

– Insufficient evidence which is material and pervasive is of such significance that the auditor is unable to state whether the financial statements give a true and fair view. – In such a situation a disclaimer of opinion is issued (e.g.: the auditors do not express an opinion on the financial statements)